We are known to be positive. Indeed, none of us can help but whom we are. We believe most if not all pig producers are positive people. You need to be. If you did a list all the reasons being a pig producer is a challenge. The list would go on and on. The risks involved relative to reward has been a challenge in almost every country the last few years.

Of course, all the challenges would be easier if profitability was available. A producer last week said to us. “I have a solution for the pig industry! We need to sell hogs for higher than the cost of production.” So true.

As an industry maybe we need to step back and assess what we need to do different. As an owner of a World Mega Producer company said to us a while ago. “We can’t just keep doing the same thing, it’s not working.”

One solution and it’s a harsh one. It’s Darwinian Capitalism. The strong survive. The prices get so low and losses so high that production gets cut prices rebound. This is what will happen in our present scenario. It’s the hog cycle. In our opinion we have been liquidating the breeding herd since spring, and it continues. Sow slaughter is up, and no doubt gilt sales are down. Sow slaughter is running in mid 60’s a week. In our opinion the U.S. is decreasing 6 – 8,000 sows a week and have been for a while.

If the lean hog futures and grain futures play out over the next 6 months as they indicate today, farrow to finish producers will lose between $20-30 per head. Over that 6 months lets estimate 60 million U.S. market hogs leading to a further $1.2 – 1.8 billion USD equity loss for the industry. This will be on top of the losses over most of the last year.

Another way to increase possibility of profitability is by increasing pork demand.

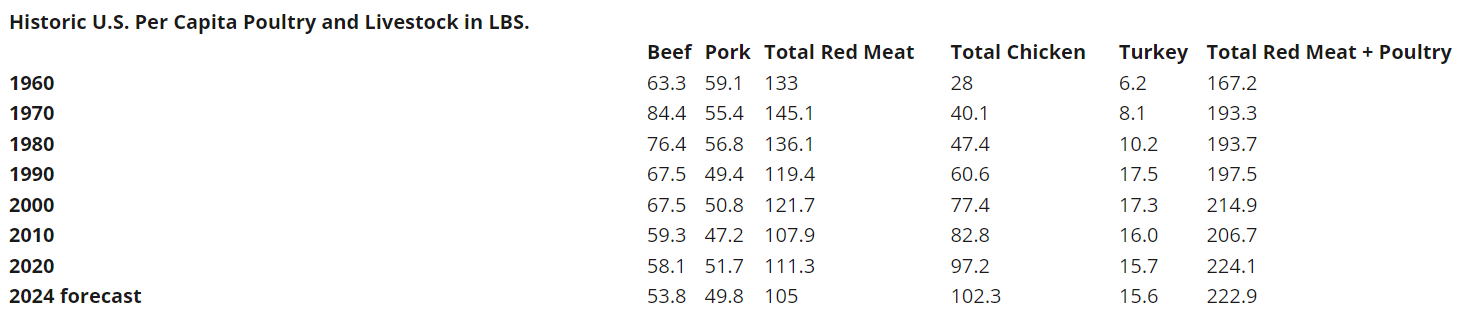

In 1960 U.S. Pork Consumption was 59.1 lbs. that was a percentage of total Red Meat and Poultry per capita consumption (167.2 lbs.) is 35%. The 2023 forecast of 53.8 lbs. as a percentage of total Red Meat and Poultry (222.9 lbs.) is 24%. The numbers are harsh no matter how you look at it. You can see on the chart that Pork per capita consumption has flatlined for 60 years. This in a market that total Red Meat + Poultry per capita consumption has increased from 167.2 lbs. to over 220 lbs.

Chicken has kicked our ass. 1960 – 28 lbs. to now over 100 lbs. per. American consumers aren’t becoming vegetarians they are eating more combined Red Meat + Poultry than ever before. Well over a billion dollars invested in Pork Checkoff by producers and we haven’t grown our business. Some don’t like us pointing this out, but it’s the grim reality. Part of our solution to profitability is demand, there is little in historical data to show Pork demand growth.

A question the industry needs to ask ourselves is why in 1960 Pork 59.1 lbs. per capita to 2024 49.8 lbs. The main driver of consumer demand is taste. Did Pork in 1960 taste better? Did the chase for ever leaner Pork destroy our consumer demand? The Other White Meat program?

There has been a loin complex task force put together by National Pork Board to see why what was a premium product is now cheaper than dog food.

Most of us know what the problem is. Many know the Pork they produce they don’t want to eat. Producers order Steak in restaurants. Many restaurants don’t have loin product on menu. Why? Customers don’t buy. Wonder how many directors, employees of Pork Board and NPPC on the producer funded per diem meals eat Pork? Eat Steak?

We all know the problem; we are producing loins that taste like crap. Until we fix it all the task forces in the world won’t change that flatlining of per capita Pork consumption and continue to contribute to financial losses.

Dog Food at $6.99 lb. vs. Pork Loin at $5.47 lb.